The COVID-19 pandemic disrupted global business operations and markets on an unprecedented scale. While many sectors faced severe economic challenges, some businesses during COVID-19 experienced accelerated growth due to shifting consumer behaviour, government support measures and rapid digital adoption.

In Australia, lockdowns in 2020 forced companies to adapt quickly. Those able to pivot their service delivery, strengthen online access, or meet non-discretionary demand were often twice as likely to improve revenue and market position.

Understanding which industries benefited from COVID-19 provides valuable insight for business owners and investors planning for future economic disruption.

If you are reassessing your strategy in light of economic volatility, Nash Advisory provides clear, evidence-based business advisory to help business owners protect and grow enterprise value.

Why some industries benefited during COVID-19

Although the COVID-19 pandemic created widespread economic disruption, it also reshaped market demand. Businesses that experienced growth during COVID-19 were often operating in sectors that aligned with new consumer constraints.

Lockdowns reduced mobility but increased household spending on goods and services. Restrictions limited physical retail but boosted online transactions. Travel declined sharply, yet domestic leisure activities increased.

Industries positively impacted by COVID-19 were typically agile, technology-enabled, or aligned with changing household priorities. This pattern reinforces a broader commercial principle: resilience often stems from business adaptation and structural positioning. In short, the pandemic did not spur growth at random. It redirected demand.

Industries that grew during COVID-19

Although the pandemic created economic challenges across global markets, several industries reported strong growth. Sector performance data from 2020 indicates that businesses operating in digital infrastructure, ecommerce, and essential services increased revenue, while discretionary sectors declined.

Industries that grew during COVID were typically those that could:

- Deliver products online

- Operate without physical proximity

- Scale quickly in response to increased demand

- Align with changing household priorities

This divergence highlights how crisis conditions can reshape competitive advantage.

IT services

The IT services industry experienced strong growth during COVID-19 as companies transitioned to remote work environments almost overnight. When restrictions forced employees to work from home, businesses had to embrace rapid digital transformation, upgrade infrastructure and protect sensitive data.

Demand increased for:

- Cloud migration and server capacity

- Cybersecurity solutions

- Collaboration platforms such as Zoom and Microsoft Teams

- Managed IT support services

Businesses during COVID-19 accelerated technology investment by several years. Companies that had previously delayed digital transformation were forced to act immediately to maintain operational continuity.

This surge in demand improved revenue across the IT services sector and highlighted the long-term importance of scalable digital infrastructure.

Online shopping and e-commerce

E-commerce surged as consumer behaviour shifted online during COVID-19. Lockdowns and social distancing restrictions affected physical retail, particularly in major CBD locations, forcing customers to purchase goods and services digitally.

Industry reports published throughout 2020 show that online sales increased by more than 50 per cent across several retail categories. In some segments, revenue growth exceeded 70 per cent as consumer demand moved rapidly away from bricks-and-mortar stores.

Australian supermarkets expanded delivery capacity, restaurants adopted online ordering, and retailers invested heavily in digital platforms. Government wage subsidy packages and stimulus measures also supported household spending, maintaining cash flow across the economy.

The result was a sustained ecommerce boom. Even as restrictions eased, surveys indicate that a high per cent of customers expect to continue purchasing products online due to convenience and broader product availability.

For many businesses during COVID-19, digital channels were no longer an additional option. They became the primary source of revenue and long-term opportunity.

Education and online learning

Online education grew significantly as remote learning became a necessity when classrooms closed during the COVID-19 pandemic. The education sector adopted online platforms to continue teaching, and demand for digital learning tools surged worldwide.

The global online education market has also expanded rapidly in monetary terms and is expected to continue growing well beyond the pandemic. Market forecasts project the online education sector to be worth tens to hundreds of billions of dollars by the end of this decade.

Recreational retail

Recreational retail benefited from shifts in lifestyle and local activity during COVID-19. With international travel restricted and many entertainment venues closed, consumers redirected discretionary spending toward outdoor and individual activities. Bike shops and golf shops experienced heightened demand as people sought exercise, personal wellbeing and safe social interaction within their local community.

Media coverage throughout 2020 highlighted product shortages as supply struggled to meet increased demand. The nature of spending changed. Rather than travel or attend large events, households focused on goods available locally. This shift had a greater effect in suburban areas than in CBD retail precincts, reinforcing the idea that behavioural change can reshape sector performance during economic disruption.

[download_industry_guides][/download_industry_guides]

Business models that perform well during economic disruption

Resilient business models perform well during economic disruption because they are built around non-discretionary demand, recurring revenue and strong cash flow management. Recession-resilient models typically provide essential goods and services, maintain diversified customer bases and prioritise business continuity planning.

Essential government services

Companies that provide services to essential government institutions such as prisons, healthcare centres, and hospitals will continue to operate and service the community regardless of the economic conditions.

These organisations tend to see an increase in activity due to community changes where increases in unemployment create more requirements for certain government-provided services. This would include service providers under the National Disability Insurance Scheme (NDIS).

Utility service providers

Companies that provide services to the utility space (electricity, water, gas) tend to fare well during recessions. Activity in these sectors tends to increase as governments look to update and upgrade infrastructure to support new jobs lost during a recession.

These businesses typically operate within regulated frameworks and long-term infrastructure models, generating recurring revenue and reducing exposure to volatility in discretionary spending.

Infrastructure and long-term public investment

Spending on large infrastructure projects is a popular way for governments to support fragile economies. Infrastructure service providers, such as engineering, construction, traffic management, and labour-hire firms, will benefit from new projects announced by governments to stimulate the economy.

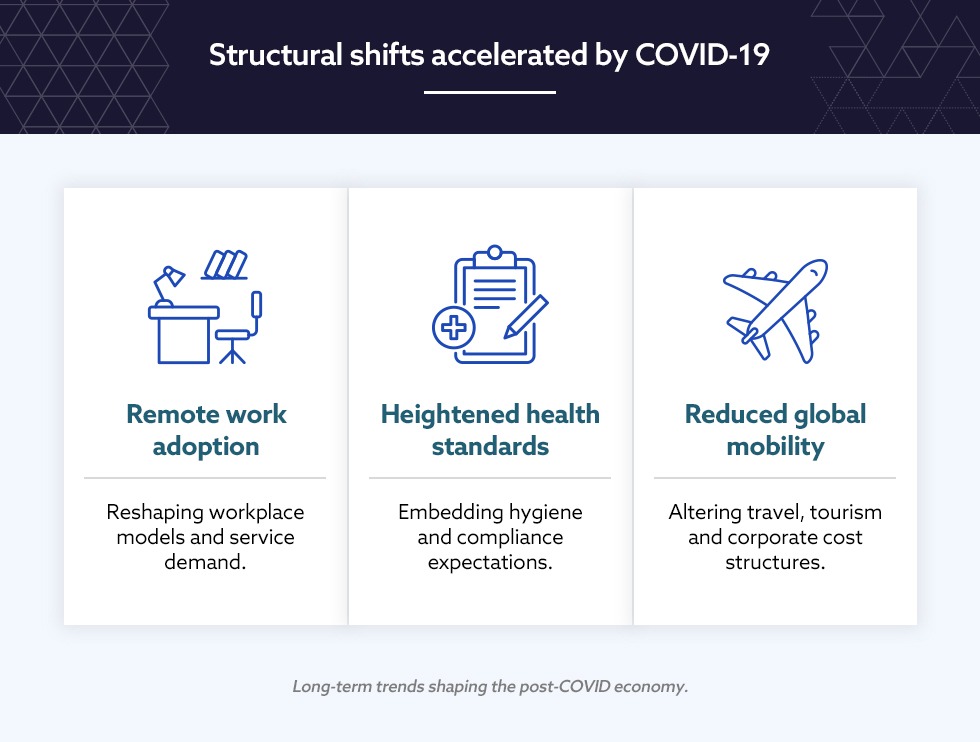

Structural themes accelerated by COVID-19

Pandemic trends accelerated long-term structural change across multiple sectors of the economy. While some shifts were temporary, others have reshaped consumer behaviour, workplace expectations and capital allocation in the post-COVID economy.

Digital adoption, flexible work, health awareness and reduced global mobility were already emerging trends prior to 2020, but the pandemic compressed years of gradual change into a short period. For business owners and investors, understanding these structural changes is critical when assessing long-term demand and strategic positioning.

The shift to working from home

Remote work adoption reshaped the workplace and service demand as organisations implemented work from home arrangements at scale. Flexible work is now embedded across many industries, influencing demand for digital collaboration tools, cybersecurity, home-office equipment, and decentralised service models.

At the same time, reduced CBD foot traffic has affected commercial property, retail and transport sectors. This shift highlights how changes in work patterns can create both opportunity and disruption across interconnected markets.

Increased focus on hygiene, safety and social distancing

Heightened awareness of hygiene and workplace safety increased demand for hygiene products and compliance services. Businesses invested in sanitisation protocols, protective equipment and revised workplace layouts to meet regulatory and community expectations.

Although restrictions have eased, the focus on risk management and health standards remains embedded in many industries. This structural adjustment supports ongoing demand for suppliers operating within the health, safety and compliance sectors.

Reduced reliance on air travel and global mobility

Reduced air travel during the pandemic altered mobility and tourism patterns both domestically and internationally. Corporate travel declined as businesses adopted virtual meeting platforms, reducing reliance on frequent interstate and international flights.

Domestic tourism benefited as consumers redirected spending to local businesses. While global mobility has partially recovered, many organisations continue to reassess travel budgets, reflecting a longer-term recalibration of cost structures and operational efficiency.

What these shifts mean for business owners and investors

Business owners and investors must adapt to post-COVID market shifts by reassessing demand drivers, cost structures and long-term growth assumptions. The future of business after the pandemic will favour companies with scalable models, strong digital capability and exposure to resilient sectors.

Investment strategy should now incorporate structural change, workforce flexibility and shifting consumer priorities rather than relying solely on historical performance. Those who proactively realign strategy are better positioned to protect enterprise value and capture emerging opportunities.

Seek business support from Nash Advisory

Nash Advisory supports strategic decision-making in the post-COVID economy by helping business owners and investors assess risk, identify opportunity and execute with clarity.

As mid-market specialists, we provide hands-on business advisory across mergers and acquisitions, capital raising and valuations, ensuring decisions are grounded in evidence and aligned with long-term value creation. In an environment shaped by structural change, disciplined strategy matters more than ever.

[internal_links_sell_business_advisors][/internal_links_sell_business_advisors]